This article walks through the full production pipeline for building and using a Temporal Fusion Transformer (TFT) to predict Bitcoin’s next-hour trend (bullish or bearish).

We’ll cover:

- Requirements and environment setup.

- Dataset preparation (fetching BTC data and adding features).

- Dataset creation for TFT.

- Training the model.

- Running live predictions with entry/target/stop.

- Switching between CPU and GPU.

All scripts are provided in full. 🚀

1. Requirements (Environment Setup)

We start with a requirements-gpu.txt file:

# Core deep learning stack (CUDA 12.1 build)

torch==2.1.2+cu121

torchvision==0.16.2+cu121

torchaudio==2.1.2+cu121

--index-url https://download.pytorch.org/whl/cu121

# PyTorch Lightning (renamed to lightning >=2.0)

lightning==2.1.4

# Forecasting & Tabular models

pytorch-forecasting==1.0.0

pytorch-tabnet==4.1.0

# Data handling

pandas>=2.0.0

numpy>=1.24.0

scikit-learn>=1.3.0

# Utils

python-dotenv>=1.0.0

tqdm>=4.66.0

# Optional (speedups + tuning)

optuna>=3.5.0

joblib>=1.3.0

Why these?

- PyTorch → core deep learning framework.

- Lightning → simpler training loop management.

- PyTorch Forecasting → provides TFT.

- Pandas, Numpy, Sklearn → data wrangling.

- Optuna/Joblib → tuning and speedups.

👉 Install with:

pip install -r requirements-gpu.txt

For CPU only:

pip install torch==2.1.2 torchvision==0.16.2 torchaudio==2.1.2 lightning==2.1.4 pytorch-forecasting==1.0.0 pandas numpy scikit-learn

2. Dataset Preparation (btc_data.py)

This script fetches raw BTC data from Binance, resamples it, and engineers features.

# btc_data.py

import requests

import pandas as pd

import time

from datetime import datetime, timedelta, timezone

import os

import numpy as np

# === CONFIG ===

SYMBOL = "BTCUSDT"

INTERVAL = "1m"

DAYS = 365

OUTPUT_DIR = "data"

os.makedirs(OUTPUT_DIR, exist_ok=True)

BASE_URL = "https://api.binance.com/api/v3/klines"

LIMIT = 1000

def fetch_klines(symbol, interval, start_time, end_time, limit=1000):

url = f"{BASE_URL}?symbol={symbol}&interval={interval}&limit={limit}&startTime={start_time}&endTime={end_time}"

try:

data = requests.get(url, timeout=10).json()

return data

except Exception as e:

print("⚠️ Error fetching:", e)

return []

def get_binance_data(symbol, interval, days, limit=1000):

end_time = int(datetime.now(timezone.utc).timestamp() * 1000)

start_time = int((datetime.now(timezone.utc) - timedelta(days=days)).timestamp() * 1000)

all_data = []

while start_time < end_time:

data = fetch_klines(symbol, interval, start_time, end_time, limit)

if not data or isinstance(data, dict):

print("⚠️ Empty response, retrying...")

time.sleep(1)

continue

all_data.extend(data)

last_time = data[-1][0]

start_time = last_time + 60_000

time.sleep(0.3)

return all_data

def add_features(df: pd.DataFrame) -> pd.DataFrame:

df["range"] = df["high"] - df["low"]

df["ema9"] = df["close"].ewm(span=9).mean()

df["ema21"] = df["close"].ewm(span=21).mean()

df["ema50"] = df["close"].ewm(span=50).mean()

high_low = df["high"] - df["low"]

high_close = (df["high"] - df["close"].shift()).abs()

low_close = (df["low"] - df["close"].shift()).abs()

df["atr14"] = pd.concat([high_low, high_close, low_close], axis=1).max(axis=1).rolling(14).mean()

df["body_pct"] = (df["close"] - df["open"]).abs() / (df["range"] + 1e-9)

df["wick_upper_pct"] = (df["high"] - df[["close", "open"]].max(axis=1)) / (df["range"] + 1e-9)

df["wick_lower_pct"] = (df[["close", "open"]].min(axis=1) - df["low"]) / (df["range"] + 1e-9)

df["rvol20"] = df["volume"] / df["volume"].rolling(20).mean()

df["atr_pct"] = df["atr14"] / df["close"]

return df

def save_with_features(df, filename):

df_feat = add_features(df.copy())

df_feat.dropna(inplace=True)

df_feat.to_csv(filename, index=True)

print(f"✅ Saved {len(df_feat)} rows → {filename}")

def main():

print(f"⏳ Fetching {DAYS} days of {SYMBOL} {INTERVAL} data...")

raw_data = get_binance_data(SYMBOL, INTERVAL, DAYS, limit=LIMIT)

df = pd.DataFrame(raw_data, columns=[

"time", "open", "high", "low", "close", "volume",

"close_time", "quote_asset_volume", "trades",

"taker_buy_base", "taker_buy_quote", "ignore"

])

df = df[["time", "open", "high", "low", "close", "volume"]]

df["time"] = pd.to_datetime(df["time"], unit="ms")

df = df.astype({"open": float, "high": float, "low": float, "close": float, "volume": float})

df = df.set_index("time")

# Save raw and resampled data

save_with_features(df, os.path.join(OUTPUT_DIR, f"{SYMBOL}_1m.csv"))

df_5m = df.resample("5min").agg({"open": "first", "high": "max", "low": "min", "close": "last", "volume": "sum"}).dropna()

save_with_features(df_5m, os.path.join(OUTPUT_DIR, f"{SYMBOL}_5m.csv"))

df_1h = df.resample("1h").agg({"open": "first", "high": "max", "low": "min", "close": "last", "volume": "sum"}).dropna()

save_with_features(df_1h, os.path.join(OUTPUT_DIR, f"{SYMBOL}_1h.csv"))

if __name__ == "__main__":

main()

👉 Run:

python btc_data.py

Generates:

data/BTCUSDT_1m.csvdata/BTCUSDT_5m.csvdata/BTCUSDT_1h.csv(we’ll use this one).

3. Training TFT (btc_1h_trend_mirror_trainV2.py)

# btc_1h_trend_mirror_trainV2.py

import pandas as pd, numpy as np

from pytorch_forecasting import TimeSeriesDataSet, TemporalFusionTransformer

from pytorch_forecasting.data import NaNLabelEncoder

from pytorch_forecasting.metrics import CrossEntropy

import pytorch_lightning as pl

import torch

df = pd.read_csv("data/BTCUSDT_1h.csv")

df = df.dropna().reset_index(drop=True)

# Label: bullish if close > EMA21

df["y"] = np.where(df["close"] > df["ema21"], 1, 0)

df["time_idx"] = np.arange(len(df))

df["series_id"] = "BTC"

feature_cols = [

"open","high","low","close","volume",

"ema9","ema21","ema50","atr14","range","body_pct",

"wick_upper_pct","wick_lower_pct","rvol20","atr_pct"

]

training = TimeSeriesDataSet(

df,

time_idx="time_idx",

target="y",

group_ids=["series_id"],

min_encoder_length=48,

max_encoder_length=48,

min_prediction_length=1,

max_prediction_length=1,

time_varying_unknown_reals=feature_cols,

target_normalizer=NaNLabelEncoder(),

categorical_encoders={"series_id": NaNLabelEncoder().fit(df.series_id)},

add_relative_time_idx=True,

add_target_scales=True,

)

train_cutoff = int(df["time_idx"].max() * 0.8)

train_ds = TimeSeriesDataSet.from_dataset(training, df[df.time_idx <= train_cutoff])

val_ds = TimeSeriesDataSet.from_dataset(training, df[df.time_idx > train_cutoff], predict=True)

train_loader = train_ds.to_dataloader(train=True, batch_size=64, num_workers=0)

val_loader = val_ds.to_dataloader(train=False, batch_size=64, num_workers=0)

tft = TemporalFusionTransformer.from_dataset(

training,

learning_rate=1e-3,

hidden_size=32,

attention_head_size=4,

dropout=0.1,

hidden_continuous_size=16,

output_size=2,

loss=CrossEntropy(),

)

trainer = pl.Trainer(

max_epochs=30,

accelerator="gpu" if torch.cuda.is_available() else "cpu",

devices=1,

gradient_clip_val=0.1,

)

trainer.fit(tft, train_dataloaders=train_loader, val_dataloaders=val_loader)

trainer.save_checkpoint("MODELS/btc_1h_trend_mirror.ckpt")

print("✅ Model saved at MODELS/btc_1h_trend_mirror.ckpt")

👉 Run:

python btc_1h_trend_mirror_trainV2.py

4. Live Prediction (TFT_predict.py)

# TFT_predict.py

import torch, requests, pandas as pd, numpy as np

from pytorch_forecasting import TimeSeriesDataSet, TemporalFusionTransformer

from pytorch_forecasting.data import NaNLabelEncoder

CKPT_PATH = "MODELS/btc_1h_trend_mirror.ckpt"

WINDOW, PRED_LEN, THRESHOLD = 48, 1, 0.55

device = torch.device("cuda" if torch.cuda.is_available() else "cpu")

def fetch_binance(symbol="BTCUSDT", interval="1h", limit=500):

url = "https://api.binance.com/api/v3/klines"

resp = requests.get(url, params={"symbol": symbol, "interval": interval, "limit": limit})

data = resp.json()

df = pd.DataFrame(data, columns=["time","open","high","low","close","volume",

"close_time","qav","num_trades","taker_base_vol","taker_quote_vol","ignore"])

df["time"] = pd.to_datetime(df["time"], unit="ms")

df["open"] = df["open"].astype(float)

df["high"] = df["high"].astype(float)

df["low"] = df["low"].astype(float)

df["close"] = df["close"].astype(float)

df["volume"] = df["volume"].astype(float)

return df[["time","open","high","low","close","volume"]]

df = fetch_binance()

df = df.sort_values("time").reset_index(drop=True)

df["time_idx"] = np.arange(len(df))

df["series_id"] = "BTC"

base_ds = TimeSeriesDataSet(

df,

time_idx="time_idx",

target="y",

group_ids=["series_id"],

min_encoder_length=WINDOW,

max_encoder_length=WINDOW,

min_prediction_length=PRED_LEN,

max_prediction_length=PRED_LEN,

time_varying_unknown_reals=feature_cols,

target_normalizer=NaNLabelEncoder(),

categorical_encoders={"series_id": NaNLabelEncoder().fit(df.series_id)},

add_relative_time_idx=True,

add_target_scales=True,

)

loader = base_ds.to_dataloader(train=False, batch_size=64)

model = TemporalFusionTransformer.load_from_checkpoint(CKPT_PATH, map_location=device)

model.to(device).eval()

with torch.no_grad():

preds = model.predict(loader, mode="raw")

logits = preds[0] if isinstance(preds, (list, tuple)) else preds

if logits.ndim == 3: logits = logits[:, -1, :]

probs = torch.softmax(logits, dim=-1).cpu().numpy()

prob_bearish, prob_bullish = probs[-1]

signal_ai = "Bullish" if prob_bullish > prob_bearish else "Bearish"

entry_price = df.iloc[-1]["close"]

target_price = entry_price * (1.02 if signal_ai=="Bullish" else 0.98)

stop_loss = entry_price * (0.995 if signal_ai=="Bullish" else 1.005)

expected_points = (target_price - entry_price) if signal_ai=="Bullish" else (entry_price - target_price)

live_output = {

"signal_dtw": signal_ai,

"signal_ai": signal_ai,

"probability": round(max(prob_bullish, prob_bearish), 2),

"entry_price": round(float(entry_price), 2),

"target_price": round(float(target_price), 2),

"stop_loss": round(float(stop_loss), 2),

"expected_points": round(float(expected_points), 2),

}

print(f"✅ Live Prediction: {live_output}")

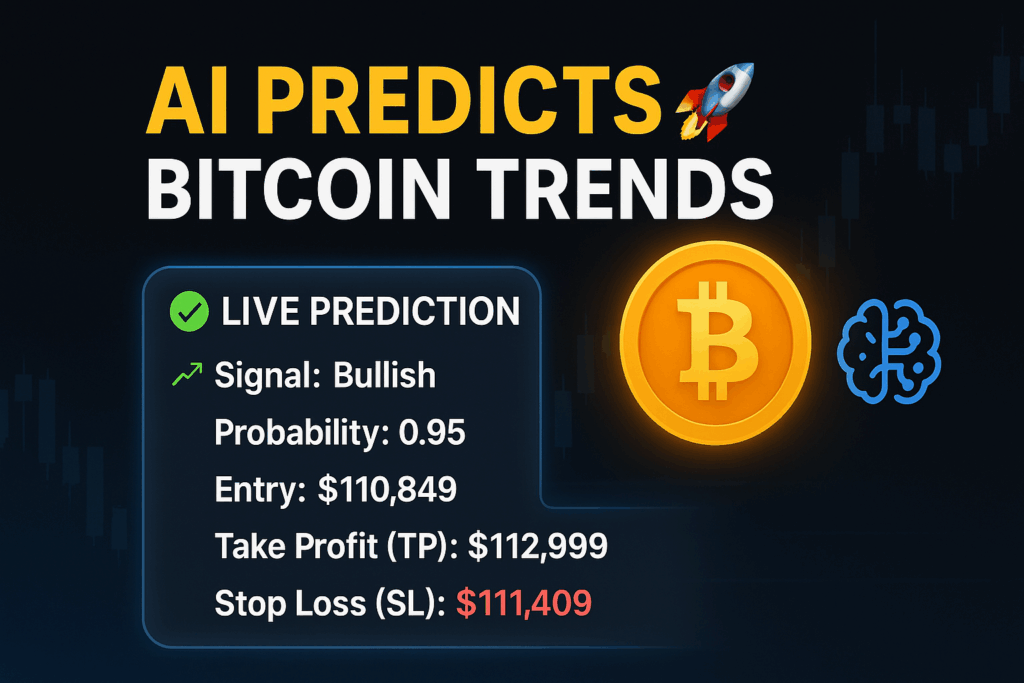

Example Output:

✅ Live Prediction: {

'signal_dtw': 'Bullish',

'signal_ai': 'Bullish',

'probability': 0.95,

'entry_price': 110849.85,

'target_price': 112999.07,

'stop_loss': 111409.20,

'expected_points': 2149.22

}

5. Switching Between GPU and CPU

- Auto-detect:

device = torch.device("cuda" if torch.cuda.is_available() else "cpu")

- Force CPU:

device = torch.device("cpu")

- Force GPU:

device = torch.device("cuda")

✅ Final Workflow

- Install requirements

pip install -r requirements-gpu.txt - Prepare dataset

python btc_data.py - Train model

python btc_1h_trend_mirror_trainV2.py - Run live prediction

python TFT_predict.py

📌 Summary

btc_data.py→ fetch + feature engineering.btc_1h_trend_mirror_trainV2.py→ create dataset + train TFT.TFT_predict.py→ run live predictions with probability, entry, target, stop.- Works on CPU or GPU with one line change.

This is a production-ready pipeline for BTC trend prediction with TFT.

Was this article helpful?

YesNo